For this fiscal year 2021, the Tax Administration Service (Servicio de Administración Tributaria) set a collection goal of 3.53 billion pesos. Audit

According to the Tax and Management Report, the Tax Administration Service (SAT) tax revenues, which include consumption taxes, corporate income taxes and workers’ income, totaled one trillion 22 thousand 47 million pesos in the first quarter of the year, an amount that exceeded by 26 thousand 198 million pesos the amount expected in the 2021 economic package.

Taking into consideration the global economic scenario resulting from the COVID-19 pandemic, achieving the collection goals of the decentralized body of the Ministry of Finance and Public Credit will undoubtedly be a task that will be promoted by making use of the broad powers of auditing.

On this occasion and because it is one of the most frequently used procedures by the tax and customs authorities at the time of auditing, we will address the most important aspects of the Field Audit in general as well as some recommendations for its due attention; clarifying that on a later occasion we will be referring to this Procedure aimed at Foreign Trade matters.

1.- FIELD AUDIT

1.- FIELD AUDIT

The Field Audit is one of the main instruments used by the tax authority (Servicio de Administración Tributaria) to check and verify the due compliance of tax and foreign trade obligations of taxpayers registered in the Federal Taxpayers Registry.

Although by its nature, it does not have collection purposes, but rather verification purposes, the reality is that, in many cases, taxpayers decide to correct their tax situation to avoid the assessment of any tax credit, and that this situation may affect them, for example, suffer a drop in the importers’ registry, or even the loss of any certification, and decide to pay the omitted taxes. Indirectly resulting in a way to increase the Collection.

This Procedure has its origin in the antepenultimate paragraph of article 16 of the Political Constitution of the United Mexican States, which establishes that the Administrative Authorities may conduct field audits to verify that the tax and/or customs provisions have been complied with, subject to the respective laws, and to the formalities prescribed for searches (with the observance of the formalities prescribed for the procedure, one of the most important Fundamental Rights is protected, which is the inviolability of the place of business).

For this reason, as this Procedure is equated, by constitutional mandate, to the formalities that must be followed in searches; Articles 42, section III, 43, 44, 45 and 46 of the Federal Tax Code provide for a detailed procedure that must be strictly observed by the authorities and that if violated, we would be facing violations ranging from procedural violations to violations of human rights, so it is important that all taxpayers know the procedure, its stages, the details of such act of inspection, as well as the form, times and means of defense that they can exercise.

2.- SUBJECTS OF THE PROCEDURE.

2.- SUBJECTS OF THE PROCEDURE.

In general, we will refer to the persons who may be subject to this type of procedure, being: individuals and legal entities, who constitutionally and directly and indirectly, are obliged to contribute to public spending, registered in the Federal Taxpayers’ Registry, obliged to pay taxes.

Likewise, those parties that must comply with the tax obligations of the taxpayer in a joint and several manner.

With respect to the persons subject to joint and several liability, it is necessary to indicate that the Federal Tax Code in its article 26, establishes that they will have this responsibility: The withholders and those responsible for collecting contributions payable by taxpayers; Those who are obligated to make provisional payments on behalf of the taxpayer; The liquidators and trustees of the company; The acquirers of negotiations; The representatives of persons not resident in the country with whose intervention these carry out activities for which contributions must be paid, companies resident in Mexico or residents abroad who have a permanent establishment in the country, among others.

3.- ACT OF INITIATION OF THE PROCEDURE – FIELD AUDIT NOTICE

3.- ACT OF INITIATION OF THE PROCEDURE – FIELD AUDIT NOTICE

The formalities that must be strictly complied with by the inspection authorities when implementing this type of procedures, verifying due compliance with tax and foreign trade obligations and even reviewing foreign merchandise, are essentially the following:

- Pursuant to the first paragraph, section III of Article 42 of the Federal Tax Code, a field audit must necessarily be initiated by means of an order, which must be in writing, as expressly provided for in Article 16 of the Constitution, first paragraph, and 38, section I of the Federal Tax Code, a document that must necessarily be issued by a competent authority, that is to say, it must be founded and justified.

- Likewise, Article 42, in its last paragraph, of the Code on the subject, indicates that the visit begins from the moment the order is notified to the person visited. For this reason, the order, by legal obligation, must be delivered personally to the person visited, or to whoever legally represents the interests of the person to whom it is addressed.

Representation, in these cases, is an important aspect, since the authority cannot initiate a visit immediately through a person who, for example, does not demonstrate legal representation or is the taxpayer sought. If the inspectors do not find the person or the person representing his interests, with a valid document, such as an Instrument before a Public Notary, they must issue a summons in order to wait for them within a fixed hour on the following business day and only in that case, the visit will be carried out with the person who appears at the time and on the day summoned. - Another important aspect is the place where the procedure must be carried out, and this will be exclusively the one indicated in the order, which is generally the taxpayer’s business address.

4.- GENERAL REQUIREMENTS OF THE FIELD AUDIT ORDER

4.- GENERAL REQUIREMENTS OF THE FIELD AUDIT ORDER

Article 43 of the Federal Tax Code categorically establishes the requirements that the field audit order must contain, which we cite below:

- The place or places where the visit is to take place. The increase in the number of places to be visited shall be notified to the visited party.

- The name of the person or persons who must carry out the visit; that is, the visiting personnel authorized to carry out the procedure.

- The period or fiscal year subject to review as well as a clear precision of the taxes or contributions that will be part of the review. The authority must conform to the object of review established in the order.

- The name of the visited party must be printed, except in the case of verification orders in foreign trade matters where the name of the visited party is unknown.

- Comply with the requirements established in article 38 of the mentioned Federal Tax Code, which are applicable for all administrative acts that must be notified, as in this case it is “the field audit order”, being the following:

- Be in writing in a printed or digital document.

- Indicate the issuing authority.

- Indicate the place and date of issuance.

- Be founded, justified and express the resolution, object or purpose in question.

- Bear the signature of the competent official.

- Indicate the name or names of the persons to whom it is addressed. When the name of the person to whom it is addressed is unknown, sufficient data shall be indicated to allow his identification.

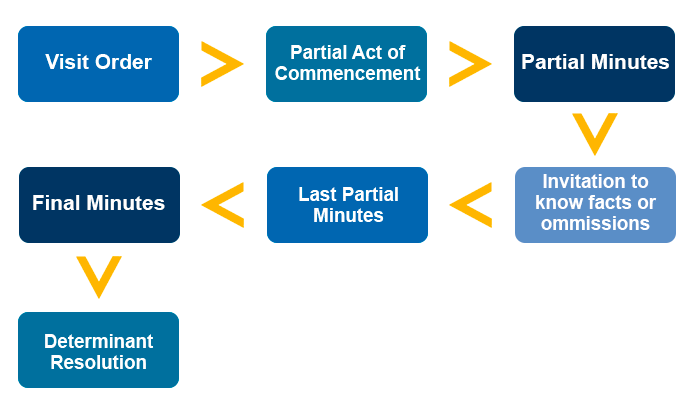

5.- MAIN STAGES OF THE FIELD AUDIT

5.- MAIN STAGES OF THE FIELD AUDIT

The Field Audit, due to its duration, is composed of several stages, which must also be carried out following the formalities established for this purpose. Below, we will refer to each of these stages:

5.1 Partial Act of Commencement.

5.2 Notification of the Field Audit

5.2 Notification of the Field Audit

This act constitutes in itself, the beginning of the field audit, with which the visitors assigned to the Authority issuing the visit order, once they are at the address indicated in the order and having previously identified themselves (in accordance with numeral 44, section III of the Federal Fiscal Code, they must identify themselves fully before the person with whom the proceeding is to take place, exhibiting an official document that accredits them as the acting personnel authorized in the order), they will request the presence of the taxpayer sought or his legal representative; If the latter is not found at the address, they will leave a summons to wait for the next business day and at a later time.

If the taxpayer is not found at the address on the day and time established in the summons, the order will be executed and the visit will begin with whoever is present, and all the actions taken since the first visit will be recorded in the “Partial Minutes of Commencement”.

5.3 Appointment of witnesses.

5.3 Appointment of witnesses.

Once the inspectors have identified themselves, they shall request the visited party to appoint two witnesses to attest to the legality of the proceedings. If the visited party refuses to appoint them, or if those appointed do not accept the position, the visitors shall do so, and shall record such circumstances in the initial minutes. If the witnesses do not appear or are absent at the time of the proceedings, or of their own free will state that they do not wish to continue with the assignment, they may be substituted by the visited party, or in the event of their refusal or impossibility, the authority will do so.

5.4. Requirement to exhibit accounting records.

5.4. Requirement to exhibit accounting records.

Once the procedure has been completed, the taxpayer or its representative shall be required to exhibit the accounting documentation subject to review, with respect to the periods and taxes included in the order.

5.5. Drawing up of the Act of initiation of the visit.

The beginning of the visit is carried out by means of a circumstantial record, where all the situations that have occurred from the beginning of the visit until the end of the visit are recorded, which must be signed by all the parties that participated in the visit, i.e.: the visitors; the taxpayer or his representative and the witnesses appointed.

5.6 Partial Minutes of Proceedings

5.6 Partial Minutes of Proceedings

In the development of the visit, for the request, reception and analysis of the documentation related to the period or fiscal year reviewed as well as the taxes and/or contributions to which the taxpayer is subject, the visitors may prepare all the partial minutes they deem pertinent. The result of the analysis of the information and/or documentation will be recorded in a special record in which the observations, facts or omissions detected will be recorded, in accordance with the provisions of number 46 of the Federal Tax Code.

If the tax authority, in the review process, considers that it must make inquiries to third parties in order to verify the veracity of the facts contained in the information and/or documentation of the taxpayer, it is mandatory that the result be made known to the visited party, otherwise such act is vitiated by illegality.

5.7 Invitation to know the facts or omissions.

5.7 Invitation to know the facts or omissions.

The last amendment to article 42 antepenultimate paragraph of the Federal Tax Code establishes a time during the visit, in which the taxpayer, his legal representative, and in the case of legal entities, their management bodies, must be notified via tax mailbox, at least 10 business days prior to the date of the last partial report, of their right to go to the offices that are carrying out the procedure in question, in order to know the facts and omissions that have been detected.

For this reason, the authority will prepare a partial record to certify the presence of the taxpayer, as well as the facts or omissions that resulted from the development of the procedure.

5.8. Last Partial and Final Report.

There are three important and mandatory reports to be taken during a field audit, one is the initial partial report, which has already been explained, the last partial report and the final report.

- When during the course of a visit the tax authorities become aware of facts or omissions that may imply noncompliance with the tax provisions, they will record them in a circumstantial manner in partial tax reports.

- When the authority is about to conclude the visit, it must draw up THE LAST PARTIAL REPORT, in which the facts or omissions detected by the visitors will be recorded, expressly granting the taxpayer a term of 20 business days, the taxpayer may present the documents, books or records that disprove the facts or omissions, as well as choose to correct its tax situation.

From the moment the Last Partial Report is issued, the taxpayer has the opportunity to exercise the fundamental right to a hearing, from which we emphasize the great importance of attending this stage in an adequate manner, providing the necessary documentation and arguments to refute the presumptions of omission or infraction made known by the authority and in itself, support full compliance with the tax and/or customs obligations reviewed.

- Once said term has elapsed, the authority will issue THE FINAL REPORT, and with said act the field audit will be formally CONCLUDED. With this we must understand that the presence of the tax authority at the taxpayer’s tax address has concluded and the authority will begin a stage in which it will evaluate and/or analyze the information and/or documentation obtained in the procedure in order to make a definitive pronouncement on the tax situation of the taxpayer visited.

The final or closing report of the audit, presumes that the procedure will be concluded taking into consideration what is stated in the last final partial report and the clarification letter of the visited party, and from there it will be concluded whether or not to determine credits to be charged to the visited taxpayer, that is, if the omissions or irregularities detected during the procedure are considered updated or disproved.

6.- Duration of the visit.

6.- Duration of the visit.

Here, we make a parenthesis to refer to the duration of this procedure, which as a general rule may not exceed 12 months from the notification of the visitation order, until the final report is issued.

Among the most common are the following cases, in which case the term to conclude the visit is suspended. To mention some of the causes for suspension of the procedure we can refer to the cases of strike; death of the taxpayer; vacating the tax address without having presented the corresponding notice of change or when the taxpayer is not located in the address indicated, until the taxpayer is located; in the event that the taxpayer does not comply with the request for data, reports or documents requested by the tax authorities to verify compliance with its tax obligations or due to impediment of the authority by fortuitous event or reasons of force majeure, until the cause is removed.

7.- Final Resolution.

7.- Final Resolution.

The issuance of the final resolution is the written act through which the taxpayer’s tax situation is formally defined, i.e., it determines compliance with tax and/or customs obligations.

The difference between the final assessment and the final resolution is that in the latter, the omission of taxes or contributions is based and motivated, according to the infringing conduct discovered during the visit, and the tax credit is determined, which is composed of the omitted taxes, fines and surcharges.

For this reason, it isn’t until the issuance and notification that the visited taxpayer or taxpayers know their real situation before the authority, and can decide what action to take.

Such resolution may be challenged through the two tax defense methods: Recurso de Revocación (Appeal for Revocation) or Juicio de Nulidad (Nullity Trial).

8.- Means of Legal Defense

8.- Means of Legal Defense

In the performance of field audits, several fundamental rights protected by the Political Constitution may be violated, such as the principles of legal security, legality, inviolability of the premises, the right to privacy, the right to banking secrecy and professional secrecy, among others; these would constitute violations of a formal nature.

And with respect to the determination of contributions or imposition of fines, cases in which there is commonly no adequate justification of the reasons why it is considered that the taxpayer incurred in the omissions or infractions sanctioned, these are commonly known as substantive violations; and to disprove them it is necessary to have suitable documentation and supporting information as well as effective legal arguments that lead to demonstrate that the taxpayer was not involved in the assumptions sanctioned by the authority; especially as advisors, we primarily focus the efforts of our legal defense strategy to these aspects and we even do it from the beginning of the field audit, in order to ensure that this does not conclude precisely in the determination of a tax credit or other legal contingencies of greater impact for the taxpayer.

Now, as mentioned above, once the final resolution has been issued, there are basically the following means of legal defense in the ordinary stage:

- Appeal for Revocation: It is filed before the SAT, within 30 days from the date of notification of the final resolution.

- Nullity Procedure: It is filed before the Federal Court of Administrative Justice, also within 30 days from the date of notification of the final resolution.

The taxpayer may choose between filing a Appeal for Revocation or a Nullity Procedure, since the term for filing is the same, however, if he/she decides to file the Appeal for Revocation and does not obtain a favorable resolution, he/she has the possibility of filing a nullity procedure, where he/she must challenge the resolution that negatively resolved the appeal, and the final resolution determining the tax credit.

It should be noted that with respect to the judgment issued in the Nullity Procedure, it may be appealed through the Direct Amparo (Direct Appeal) Procedure and this will be the last opportunity for the taxpayer’s defense.

9.- General Recommendations for the Field Visit.

9.- General Recommendations for the Field Visit.

Based on the above, we suggest implementing the following preventive, control and corrective measures to successfully deal with this type of procedure:

- Avoid filing zero returns if income was earned.

- Constantly monitor the status of CFDI’s received from suppliers and creditors.

- Timely submit tax obligations and keep all receipts or records in safekeeping.

- Actively review your tax mailbox, since this means of communication will be the channel for communicating the facts or omissions detected in the procedure.

- To comply in a timely manner with the information and/or documentation requirements of the tax authority, as the case may be.

- Exercise the right of defense in a timely manner and be informed of the facilities or correction measures.

- To give an adequate follow-up of the acts that are carried out in charge.

- To give an adequate follow-up of the acts that are carried out in charge.

- Exhibit or provide only the information and/or documentation that is required by the authority.

- Regardless of how simple it may seem to solve, it is recommended to seek expert advice from the beginning of the field audit, since many of the unfavorable results obtained at the conclusion of this type of procedure come from the implementation of incompatible or inadequate decisions or strategies that are taken by not knowing the scope of the information and/or documentation with which the acts of the audit authority are generally solved.

10.- How can we support you at Stratego Asesores?

10.- How can we support you at Stratego Asesores?

Our group of professional experts in Legal, Fiscal and Foreign Trade matters will offer their support and experience in the handling of this type of procedure, providing:

- We provide timely legal advice on tax and foreign trade matters, designing effective strategies from the beginning of the procedure to successfully deal with the audit.

- We focus on ensuring an active and specialized attention and follow-up during the administrative procedure, ensuring in most cases, its favorable conclusion in the administrative instance (Field Audit), avoiding prolonged litigation, with costly contingencies and high legal impact for the taxpayer.

The peace of mind of our clients is the result we achieve through the professionalism of our team, who with each case and each defense, use their extensive experience and knowledge to attend each matter closely with: Commitment, Efficiency, Integrity and honesty.

This document does not constitute a particular consultation, and therefore Asesores Stratego S. C., is not responsible for the interpretation or application granted. We are in your service to respond to any questions or comments. For more information regarding this subject and our services: info@asesores-stratego.com

responsible for the interpretation or application granted. We are in your service to respond to any questions or comments. For more information regarding this subject and our services: info@asesores-stratego.com